The Record That Nobody Thought Was Possible

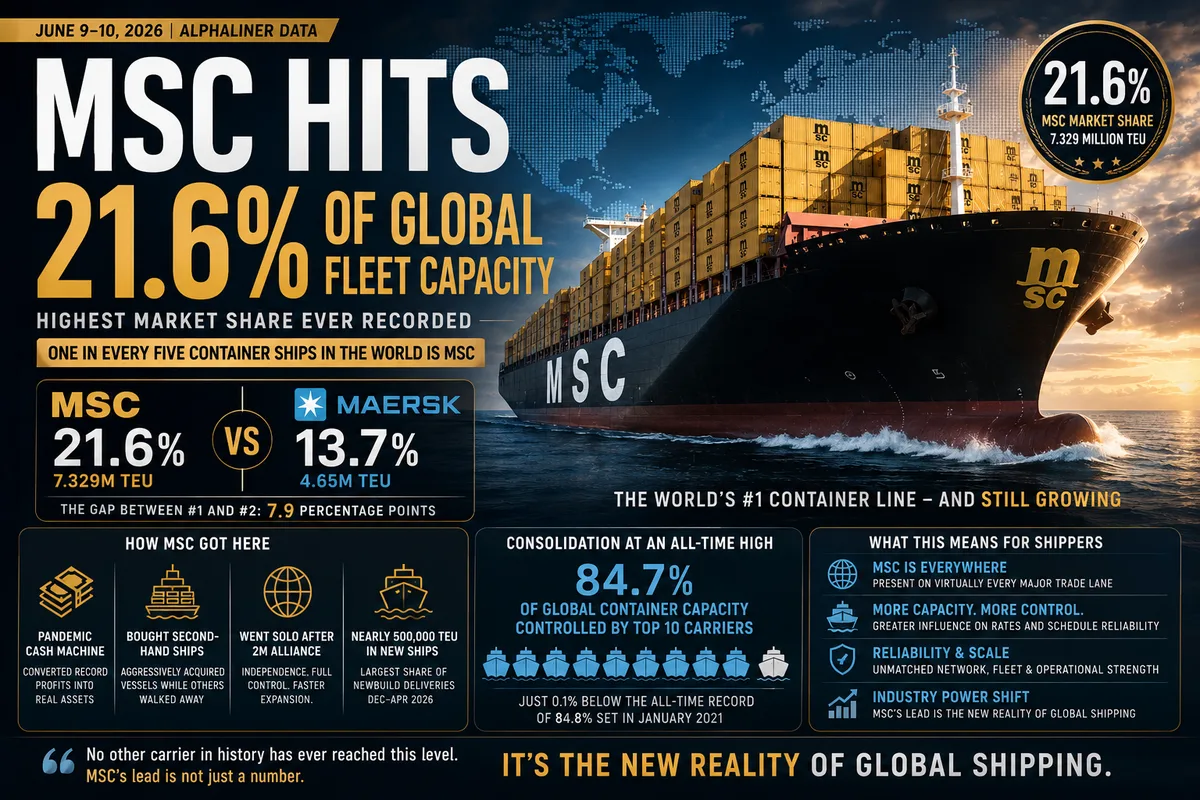

According to Alphaliner's most recent data published June 9-10, 2026, MSC Mediterranean Shipping Company has reached 21.6% of global container fleet capacity — the highest market share ever recorded by a single container carrier in the history of the shipping industry.

To put that in simple terms: if you put all the container ships in the world end to end, more than one in every five of them belongs to MSC.

The previous record was held by Maersk — which reached 19.3% market share in 2018 during its aggressive consolidation strategy. MSC has now beaten that record by more than two full percentage points. No other carrier has ever come close to these levels.

And the number is still growing. MSC's fleet has expanded to 7.329 million TEU — meaning it can carry 7.329 million standard 20-foot containers at once across its global network.

How Did MSC Get Here So Fast?

MSC's rise from a solid mid-tier carrier to the undisputed dominant force in global container shipping is one of the most remarkable corporate stories in logistics history. Here is how it happened:

Step 1: The Pandemic Cash Machine (2020-2022)

When COVID-19 hit in 2020, it created the greatest shipping boom in history. Container rates went from around $1,500/FEU to over $15,000-$20,000/FEU on some routes. Every container shipping company made enormous profits. But while most carriers used those profits for dividends and share buybacks, MSC did something different — it used the cash to buy ships. Lots and lots of ships.

MSC's strategy was built on a tactic that its rivals opted not to emulate: converting pandemic-era cash flow into tangible assets at a speed and magnitude that none of its competitors were willing or able to match.

Step 2: Buying Second-Hand Ships When Nobody Else Would

MSC was not just ordering new ships from shipyards — it was also buying second-hand vessels aggressively. In 2021 and 2022, when older ships were available at what turned out to be very attractive prices, MSC was the buyer of last resort for dozens of vessels. Its competitors thought those older ships were too costly to run. MSC thought they were a bargain.

Step 3: Going It Alone After the 2M Alliance

Until early 2025, MSC had been partners with Maersk in the "2M Alliance" — the world's largest shipping alliance. When that alliance broke up in early 2025 and Maersk partnered with Hapag-Lloyd in the new "Gemini Cooperation," MSC chose a completely different path: independence. No alliance, no partners, no sharing of ships.

Going independent meant MSC had to operate its entire global network on its own ships — which pushed it to accelerate fleet expansion even further. The strategy appears to be working: MSC's market share has grown significantly since it went independent.

Step 4: Nearly 500,000 TEU in New Ships Just This Year

Nearly 500,000 TEU in newbuilding tonnage was handed over to the top ten carriers in the December-April 2026 period — and MSC received the largest share. This massive injection of new ship capacity is what pushed MSC above 21% market share this spring.

Maersk Going the Other Direction — Down to 13.7%

While MSC has been expanding aggressively, Maersk has been doing almost the exact opposite. Maersk has fallen to a 20-year low of 13.7% global market share.

Why? Maersk made a deliberate strategic choice. The Danish shipping giant decided several years ago to cap its container fleet at around 4.1-4.3 million TEU and pivot its business toward becoming an end-to-end logistics provider — not just a shipping line. Maersk has been investing heavily in warehouses, trucking companies, customs brokers, and digital platforms instead of ordering more ships.

It is a bold strategy — but the market share numbers show the cost. Between 2018 (when Maersk had 19.3% market share) and today (13.7%), Maersk has lost 5.6 percentage points of market share. Meanwhile MSC has gained enormously.

The gap between MSC and Maersk — the world's #1 and #2 container carriers — is now 7.9 percentage points. That is an enormous gap in a market where the top carriers used to be closely bunched together.

The Top 10 Carriers Now Control 84.7% of All Container Capacity

The MSC story is dramatic — but it is part of an even bigger trend: the entire container shipping industry is becoming more and more concentrated.

The ten largest container carriers collectively now control 84.7% of global container capacity — just 0.1 percentage points below the all-time record of 84.8% set in January 2021 at the height of the pandemic.

Here is what that means in plain English: ten companies control almost 85% of all the container shipping capacity in the world. The other 15% is shared among dozens of smaller regional carriers.

Is this a problem? Industry publication The Loadstar asked exactly this question this week: "Have container shipping lines simply become too big to fail?" The question is not just academic. When a handful of very large carriers control most of the world's shipping capacity, they have enormous pricing power — and shippers have very few alternatives when those carriers decide to raise rates simultaneously, as we have seen repeatedly in 2026.

What Does MSC's 21.6% Market Share Mean for Shippers?

For freight forwarders, importers, and logistics managers, MSC's dominant market position has several practical implications:

- MSC is now unavoidable on most trade lanes. With 21.6% of global capacity, MSC operates on virtually every major shipping route in the world. If you are booking ocean freight, you are almost certainly either booking with MSC directly or being offered MSC vessels through your freight forwarder.

- MSC's pricing sets the market tone. When a single carrier controls more than one in five container ships, its rate decisions carry enormous weight. When MSC raises rates — as it did aggressively in June 2026 — the rest of the market tends to follow. There is simply not enough alternative capacity to put meaningful competitive pressure on MSC's pricing.

- MSC going independent means no alliance safety net. Under the old 2M Alliance, if MSC had a problem, Maersk's ships could potentially fill gaps. Now that MSC operates independently, any disruption to MSC's network — a major port call change, a technical problem with a vessel series, a geopolitical issue affecting a key route — could have significant implications for shippers who rely heavily on MSC sailings.

- More vessel capacity is actually good news for shippers in the medium term. In the short term, carriers are using tight capacity to push rates higher. But the massive fleet expansion by MSC, CMA CGM, and others means significant new capacity is coming to market — which will eventually put downward pressure on rates when the peak season ends.

The Concentration Question — Is This a Problem for the Industry?

The fact that 10 carriers now control 84.7% of global container capacity raises serious questions about competition and market power. Here is how different groups see it:

- Shippers say yes, it is a problem. Shipping industry groups representing importers and exporters have been arguing for years that the consolidation of the carrier market gives shipping lines too much pricing power. The pandemic-era rate spikes — which saw some shippers paying 10-15 times normal rates — were partly a consequence of this concentration.

- Regulators are watching. The US Federal Maritime Commission (FMC) and the European Commission have both been investigating carrier pricing practices. The FMC's recent fines against MSC ($22.67 million) and Maersk ($1.9 million) for detention and demurrage violations are part of a broader pattern of regulatory scrutiny of the large carriers.

- Carriers argue efficiency benefits shippers. Larger carriers can invest more in efficient vessels, port infrastructure, digital systems, and environmental upgrades — which they argue ultimately benefit shippers through better service and lower long-term costs.

Key Takeaways — June 14, 2026

- MSC has reached 21.6% global container market share — the highest ever recorded by any carrier in history. (Alphaliner, June 9, 2026)

- The previous record was Maersk's 19.3% in 2018 — MSC has beaten it by 2.3 percentage points.

- MSC's fleet: 7.329 million TEU — effectively doubling its market share since 2010.

- Maersk has fallen to 13.7% — a 20-year low — as it deliberately caps fleet growth to focus on logistics services.

- The gap between #1 MSC and #2 Maersk: 7.9 percentage points — the widest ever.

- Top 10 carriers now control 84.7% of global container capacity — approaching the all-time record.

- MSC operates independently — no alliance partnerships — running its entire global network on its own ships.

- For shippers: MSC is now unavoidable on most routes, its pricing sets the market tone, and its decisions affect everyone in ocean freight.

MSC started in 1970 as a single-ship operation founded by an Italian captain. It is now the most dominant container shipping company in the history of the industry — controlling more than one in five container ships on earth. The pace at which it has achieved this dominance — especially since 2020 — is without precedent in shipping history. For every freight forwarder, shipper, and logistics professional, understanding MSC's scale and market power is no longer optional. It is essential.

Comments

No comments yet. Be the first to share your thoughts!

Join the conversation

You need an account to comment on articles.